Blog

When the Giants Shift: What Citrix and VMware’s Strategy Means for Everyone Else

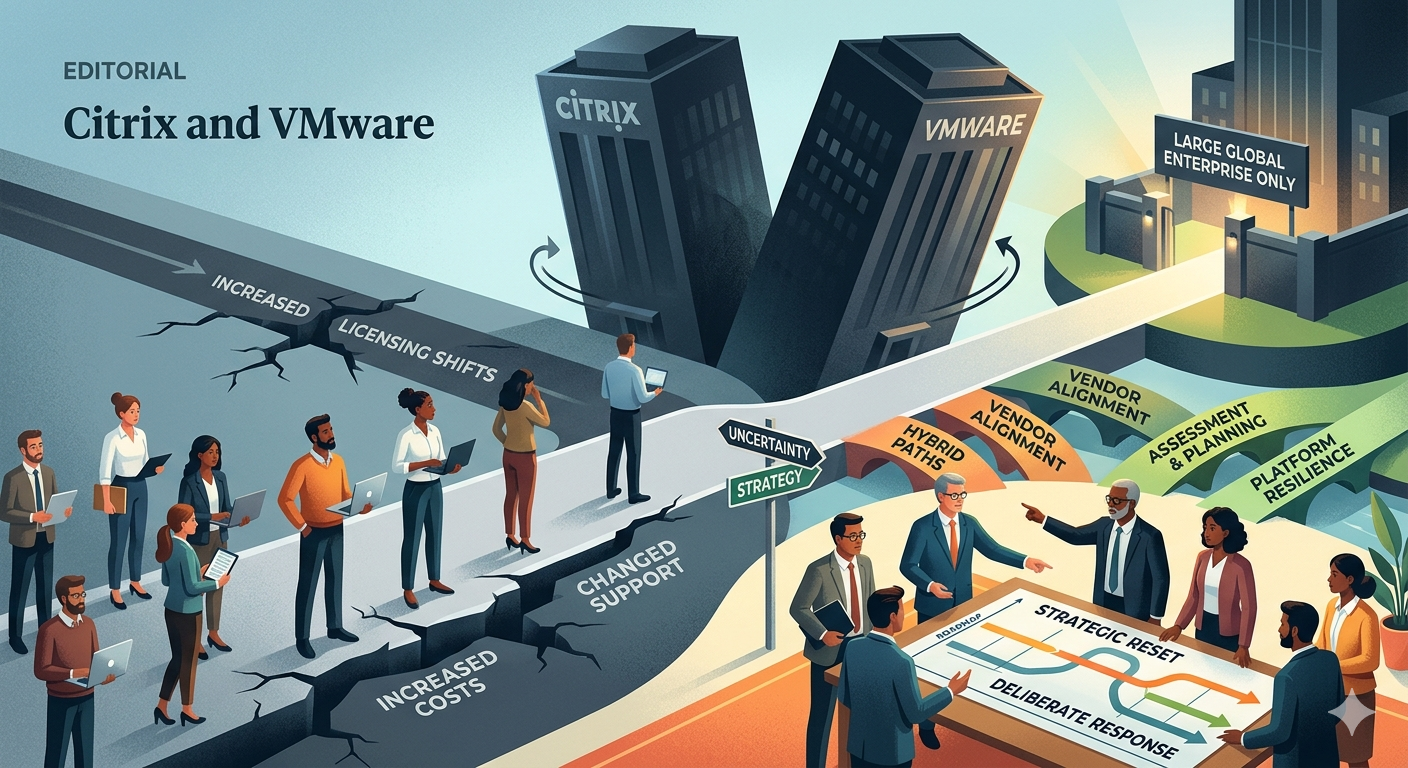

For years, IT leaders built their environments on platforms like Citrix and VMware with confidence. They weren’t just vendors; they were foundational infrastructure. Predictable licensing, strong partner ecosystems, and dependable support made them safe long-term bets.

But over the past few years, something changed.

Quietly at first, and then very publicly both Citrix and VMware began reorienting around large enterprise customers. Licensing models shifted. Support models evolved. Partner engagement changed. And for many organizations outside the global enterprise tier, the experience feels fundamentally different today.

Not broken. Just different.

And that difference is forcing a strategic reset across much of the market.

What Actually Changed

1. The Enterprise-First Pivot

Both vendors moved aggressively toward enterprise consolidation:

- Simplified, but significantly more expensive bundled licensing

- Higher minimum commitments

- Fewer flexible purchasing paths

- Dedicated focus on global strategic accounts

From a business standpoint, the move makes sense. Predictable recurring revenue, margin pressure, investor expectations, and operational efficiency all point in the same direction: fewer customers, larger deals.

But for organizations with roughly 500 to a few thousand users (large enough to be complex, but not large enough to command enterprise attention) the shift created friction.

Costs rose. Influence declined. Flexibility narrowed.

2. The Channel and Support Experience Evolved

Historically, partners played a central advisory role across licensing, architecture, and lifecycle management. Today, engagement is more centralized and vendor-direct, and smaller organizations often struggle to access meaningful support depth.

Common themes we’re hearing across industries:

- Longer response and resolution cycles

- Less consistent escalation paths

- Fewer engineers experienced with complex legacy estates

- Delays in quoting, renewals, and licensing clarity

For organizations running stable but aging environments, the pressure is real: modernize faster than planned, pay more to maintain status quo, or accept increased operational risk.

3. Strategic Pressure Arrived All at Once

The real disruption isn’t just cost, it’s timing.

Across healthcare, manufacturing, regional financial services, and public-sector environments, leaders are navigating:

Budget shock: Renewals arriving with significant increases and limited optimization guidance

Strategic fatigue: Roadmap decisions being forced earlier than expected

Skills pressure: Teams supporting legacy stacks while learning modern architectures simultaneously

Decision paralysis: Caught between staying put, replatforming under pressure, or adopting temporary hybrids

For many, it feels less like evolution and more like acceleration.

Why the Vendors Are Doing It (And Why It Still Hurts)

To be fair, this shift isn’t random, it’s structural.

Large platform vendors are responding to:

- Investor demand for recurring revenue and margin expansion

- Cost pressure from supporting fragmented legacy estates

- Competitive pressure from hyperscalers

- The economics of operating at enterprise scale

Focusing on large global accounts is logical from their perspective.

But logical doesn’t mean painless for everyone else.

What Smart Organizations Are Doing Instead

The strongest IT organizations aren’t reacting emotionally. They’re responding deliberately.

We consistently see leaders taking four practical steps:

1. Assess Before Acting

They start with licensing, cost, and architecture assessments to understand true exposure before making large commitments.

2. Separate Emotion from Architecture

Not every workload requires immediate change. Stability still has value.

3. Explore Hybrid Paths

Many are diversifying strategically:

- Citrix control planes with flexible delivery models

- VMware rationalization instead of full exit

- Nutanix adoption for targeted workloads (helped by aggressive migration incentives)

4. Reevaluate Vendor Alignment

More organizations are asking a simple but overdue question:

Does this vendor still align with our size, growth path, and operating model?

The Opportunity Inside the Disruption

Despite the frustration, the shift is forcing long-overdue conversations around:

- Technical debt and lifecycle discipline

- Vendor concentration risk

- Platform resilience and flexibility

- Governance across infrastructure, cloud, and emerging AI workloads

For many organizations, this moment is less about replacement and more about recalibration.

What Comes Next

Citrix and VMware didn’t intentionally abandon the broader market. They evolved toward where they see growth, and every evolution leaves gaps behind.

The organizations that navigate this shift best won’t be the ones that move fastest.

They’ll be the ones that move most deliberately, grounding decisions in architecture, cost clarity, and long-term resilience rather than urgency.

And in this cycle, strategy matters more than speed.

TCC is here to help as we have been for many of these cycles – reach out to us at https://www.thinclient.net/contact-us

Let's discuss a strategic IT partnership today!